Many Americans living overseas assume that “I live abroad, I don’t owe U.S. tax.” That belief trips up more expats than any single misunderstanding about visas or healthcare. The plain answer is: quite often you still must file a U.S. federal return and report worldwide income if your gross income hits the filing thresholds, and separate reporting rules reach deep into your foreign bank accounts and other assets.

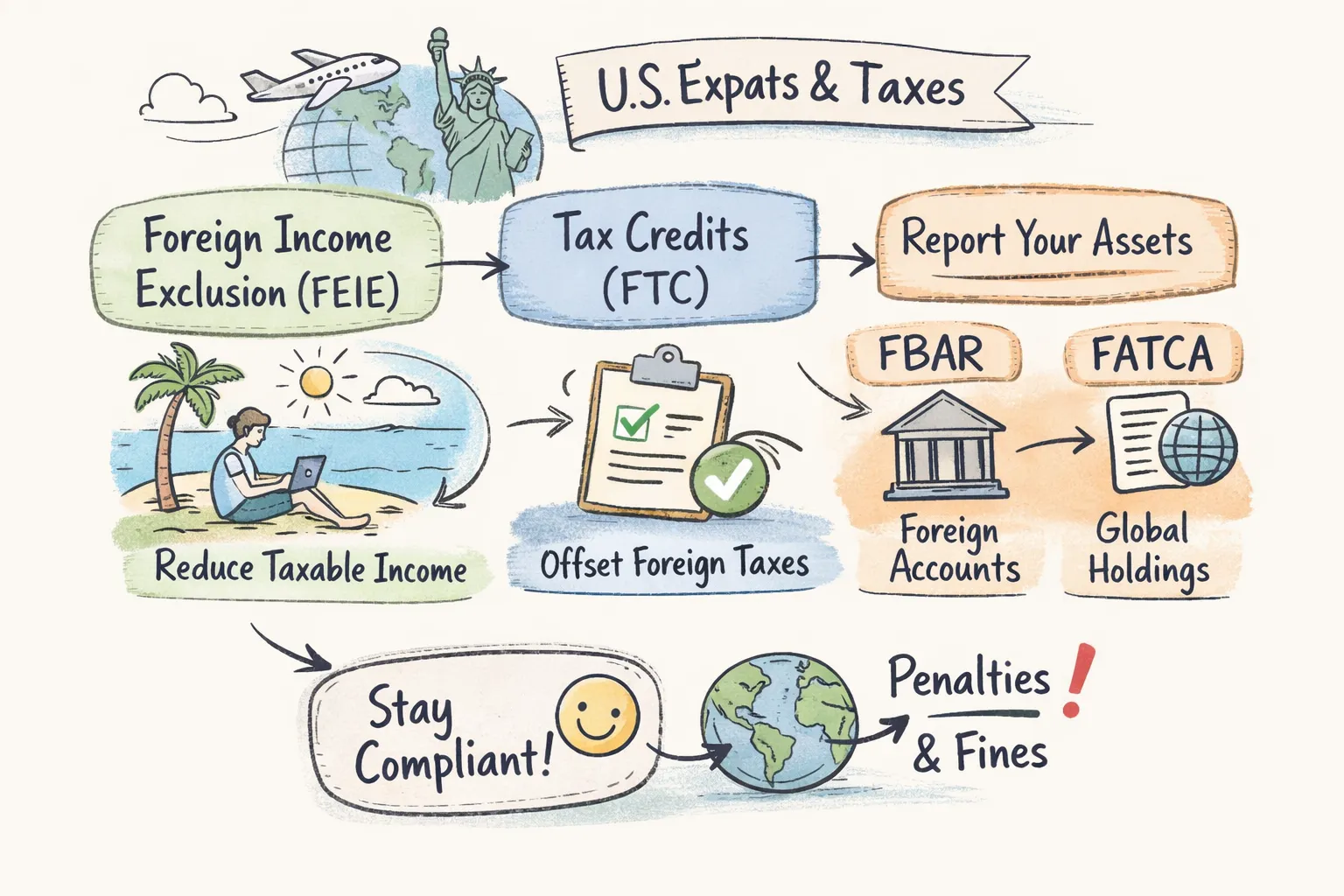

Here’s the quick map: start by asking whether your worldwide income exceeds the filing thresholds for your filing status (there are special low thresholds for spouses and for self-employment). If you must file, your two main tax‑minimizing choices are the Foreign Earned Income Exclusion (FEIE, Form 2555) and the Foreign Tax Credit (FTC, Form 1116). Separate reporting regimes—FBAR (FinCEN Form 114) and FATCA (Form 8938)—cover foreign accounts and non‑account assets and can carry steep penalties if ignored. Self‑employment tax and state tax residency are separate traps that FEIE won’t fix.

At Expats World we see the same mistakes again and again: missed filings, misapplied FEIE, and forgotten FBARs. This guide is a concise playbook: who must file, how to choose FEIE vs. FTC, what account reports you must send, practical filing steps, and a 30‑day plan you can act on today. Keep your documents ready—these rules reward good records.

Do you have to file U.S. taxes while living abroad?

U.S. citizens are taxed on worldwide income because the U.S. uses citizenship-based taxation. Whether you must file depends on your gross worldwide income, filing status, and age. For the 2025 tax year (returns filed in 2026) filing thresholds fall in the mid‑range: expect roughly mid‑$15k for a single filer under 65 and roughly $30k–$31.5k for married filing jointly (exact amounts are inflation‑adjusted every year—check IRS guidance before filing). Importantly, self‑employed persons must file if net earnings are $400 or more.

“Worldwide income” means more than wages: it includes salaries, self‑employment income, pensions, rental and investment income, and certain noncash payments. Even income you later exclude with FEIE must be shown on your return to claim the exclusion.

Decision filter (one‑line tree): Are you a U.S. citizen or resident? Is your total gross income above the filing threshold for your status, or did you earn $400+ in self‑employment income, or do you have foreign accounts/assets that trigger reporting? If yes to any, gather documents and read on.

Example: a single teacher in Lisbon earning $36,000. She must file because her worldwide gross exceeds the filing threshold. If she qualifies for FEIE (bona fide resident or 330‑day physical presence), she may be able to exclude most or all of her $36k from U.S. income tax—but she must still file Form 1040 with Form 2555 to claim it, and she must check FBAR/FATCA thresholds for bank accounts.

FEIE vs. Foreign Tax Credit: which path saves you money?

FEIE and the Foreign Tax Credit are different tools for different problems. Summarized plainly: FEIE removes qualifying foreign earned income from U.S. income tax up to the annual limit if you meet tax‑home and residency/physical presence tests. FTC gives a dollar‑for‑dollar credit for foreign income taxes you actually paid, preventing double taxation on the same income.

How FEIE works (Form 2555)

To use FEIE you must have foreign‑earned income, a tax home in a foreign country, and pass either the bona fide residence test (residence of an uninterrupted tax year in a foreign country) or the physical presence test (330 full days in any 12‑month period). FEIE covers wages and self‑employment earnings (earned income), but not passive income such as dividends, interest, or rental income. For tax year 2025 the FEIE limit is $130,000 per qualifying person (rising in later years); amounts above that remain taxable.

Document the tests. For the 330‑day test keep boarding passes, flight itineraries, rental/lease dates, and work contracts. For bona fide residence track local ties: local tax payments, long‑term lease or property, family or social integration, and an intent to remain.

See more on the Foreign Earned Income Exclusion for practical tips and recent updates.

How the Foreign Tax Credit works (Form 1116)

The FTC lets you credit qualifying foreign income taxes against your U.S. tax on the same income. Form 1116 asks you to place income into categories (general, passive, etc.), calculate the U.S. tax attributable to foreign‑source income using the limitation formula, and then apply the lesser of foreign taxes paid or the allowed limit. Unused FTCs can generally be carried back one year and forward up to ten years.

Use FTC when foreign tax rates are high relative to U.S. rates, when you have passive foreign income, or when you want to preserve a credit carryforward. FEIE often wins in low‑tax jurisdictions where excluding wages eliminates U.S. tax entirely; FTC often wins in high‑tax countries because it preserves the value of taxes you paid.

| Situation | When FEIE usually helps | When FTC usually helps |

|---|---|---|

| Tax rate on foreign wages | Low or zero foreign tax; exclude wages to avoid U.S. tax | High foreign tax rate—credit preserves tax paid |

| Type of income | Earned wages/salary only | Passive income, investment income, or mixed income |

| Carryover needs | No carryover (exclusion only) | Unused credit can carry back/forward |

| Self‑employment | Does not reduce self‑employment tax | Credits foreign income taxes but not self‑employment tax |

Short numeric illustration: if you earn $150,000 in a country with a high income tax, the foreign taxes you pay may produce a larger FTC that eliminates most U.S. tax. If you earn $60,000 in a tax‑friendly country, excluding $60k under FEIE may leave you with $0 U.S. income tax. Run both calculations annually: FEIE reduces the income base used to compute the FTC, so the order and math matters.

Married filers: each spouse can claim FEIE separately if both qualify. If one spouse uses FEIE and the other uses FTC, coordinate allocations carefully—mistakes create lost credits.

FBAR and FATCA: foreign accounts and asset reporting explained

Reporting foreign financial holdings involves two parallel regimes. FBAR (FinCEN Form 114) is a Treasury filing about foreign financial accounts; FATCA (Form 8938) is an IRS attachment to your tax return about specified foreign financial assets. They overlap but neither replaces the other.

FBAR triggers when the aggregate maximum value of your foreign financial accounts exceeds $10,000 at any time during the calendar year. “Any time” matters: a single high balance in July triggers a requirement even if December balances are low. FBAR covers bank accounts, brokerage accounts, some pensions and cash‑value insurance, and accounts where you have signature authority. File electronically via FinCEN’s BSA E‑Filing system; FBAR is not attached to Form 1040.

For a practical overview see FBAR compliance: reporting your foreign bank accounts.

FATCA (Form 8938) has higher, status‑based thresholds and a broader asset scope that can include foreign stock holdings, interests in foreign corporations and partnerships, and certain foreign pensions. Thresholds are larger for taxpayers living abroad, but if your aggregate specified foreign assets exceed the FATCA limit you must include Form 8938 with your Form 1040.

Penalties are real. FBAR non‑willful penalties can reach into the tens of thousands per violation (inflation‑adjusted), and willful violations carry far larger penalties—generally the greater of a sizable statutory amount or a percentage of the account balance. FATCA penalties start at a $10,000 base and can climb if you ignore IRS notices. File both forms when required; filing one does not absolve the other.

Filing tips: identify the maximum balance for each account during the year and convert to USD using the Treasury/IRS exchange rate guidance; keep statements that show max balances. If you discover a late or missed FBAR or 8938, document the omission and consider prompt voluntary remediation options—streamlined procedures exist for non‑willful cases, but professional help is essential when willfulness might be at issue.

Self‑employment abroad: Social Security, Schedule SE, and totalization agreements

If you are self‑employed abroad you generally owe self‑employment tax (Social Security + Medicare) on net earnings of $400 or more. The combined self‑employment rate is 15.3% (12.4% Social Security up to the applicable wage base and 2.9% Medicare on all net earnings). For 2025 the Social Security portion applies to the first approximately $176,100 of net earnings (check current SSA tables each year).

FEIE does not erase self‑employment tax. Even if you exclude foreign earned income on Form 2555, you still calculate and pay Schedule SE unless a totalization agreement applies. Totalization agreements between the U.S. and some countries prevent double contributions to two social security systems; if you are covered by the foreign system you can obtain a Certificate of Coverage from the SSA to exempt you from U.S. contributions.

Practical steps: if you’re a contractor, determine where payroll and social security obligations land (your country, a U.S. client, or a seconded employer). If you think a totalization agreement applies, request the Certificate of Coverage early—administrative delays happen. File Schedule SE with your return and keep payroll records that show which system you paid into.

When to consult a pro: if you have mixed U.S./foreign work, multiple employers, or are considering corporate structures to change payroll exposure—these decisions can materially change self‑employment tax outcomes.

State taxes and domicile traps: severing ties the right way

Federal and state taxes are separate beasts. Leaving the U.S. doesn’t automatically end state tax residency; many states use domicile or “ties” tests and continue to assert tax claims if you retain significant connections. States that frequently audit former residents include New York, California, and New Jersey, but any state can challenge residency status.

To establish non‑residency practically, reduce and document your U.S. ties. Typical steps: change voter registration, surrender or replace your driver’s license with a local one, sell or rent out your U.S. home and keep the lease, move primary banking to local institutions, and save a foreign employment contract or long‑term lease. Keep a clear paper trail: foreign utility bills, local tax returns, passport entry/exit stamps, and proof of family relocation or local school enrollment are persuasive.

Example trap: a remote worker moves abroad but keeps a U.S. home, U.S. social clubs, and family stays behind. States can argue domicile never changed. If you retain property, ongoing U.S. healthcare or other ties, get state‑tax advice. Documentation is your defense in audits.

Deadlines, forms, and a practical filing workflow

Know the forms and where they go: Form 1040 to the IRS; Form 2555 to claim FEIE or Form 1116 to claim FTC (attach to 1040); Schedule SE for self‑employment tax; Form 8938 filed with your return for FATCA; and FinCEN Form 114 is filed electronically to FinCEN for FBAR. Use Form 4868 if you need a filing extension beyond the expat automatic extension. For official filing thresholds and guidance see the IRS filing requirements for U.S. citizens and residents abroad.

Key dates to bear in mind: April 15 is the standard filing and payment deadline; U.S. citizens living and working abroad get an automatic filing extension to June 15 (you must file to claim it; interest still accrues on unpaid tax from April 15). File Form 4868 to extend the filing due date to October 15. FBAR has an automatic extension to October 15 as well. Estimated tax payments still follow quarterly schedules—avoid penalties by making timely payments or adjusting estimated amounts.

Practical six‑week workflow before filing:

- Gather documents: paystubs, foreign tax returns, employer letters, bank/brokerage statements, passports, lease/purchase agreements.

- Compute worldwide income in USD and run FEIE vs FTC scenarios for the year.

- Prepare Form 1040 with the applicable schedules and attach 2555 or 1116 and Schedule SE if needed.

- File FBAR online via BSA E‑Filing before the FBAR deadline; attach Form 8938 to your return if thresholds are exceeded.

- Make estimated tax payments if you expect tax due and keep backups of filings and confirmations.

Document checklist to gather now: recent paystubs and year‑end wage statements; the foreign country tax return and proof of taxes paid; employer letters confirming work location and tax home; bank and brokerage statements showing highest balances for the year; passport pages showing travel dates; lease or property purchase documents; and business receipts if self‑employed. Keep these records for at least six years.

Currency conversions: use IRS/Treasury guidance for converting foreign currency to USD on your return and for FBAR balances. Follow the prescribed rates—conversion method matters on audited items.

Common pitfalls, audit triggers, and how to fix mistakes

Common errors we see: assuming no U.S. filing required simply because you live abroad; miscounting physical presence days for the 330‑day test; applying FEIE to passive income (it doesn’t apply); and overlooking FBAR because each account alone seemed small but the aggregate exceeded $10,000. Also, don’t assume FEIE handles state taxes.

Audit red flags include inconsistent reporting between Form 8938 and FBAR, claiming unusually large foreign tax credits compared with U.S. liability, large refunds, or sudden transfers of funds near filing time. These patterns prompt more detailed IRS scrutiny.

If you missed filings: stop the clock by assembling records immediately—bank statements, tax returns filed abroad, payroll records, and passport stamps. For non‑willful omissions the streamlined filing compliance procedures (or late‑filing remedies) may mitigate penalties; suspected willfulness raises the stakes and warrants urgent professional help. Never ignore IRS or FinCEN notices—responding promptly reduces exposure.

Preventive checklist (annual habits): keep monthly statements in a single encrypted folder; calendar an annual “expat tax day” to run FEIE/FTC scenarios; record travel dates contemporaneously; and reconcile FBAR/FATCA thresholds before year‑end.

Next steps, tools, and when to call a tax professional

30‑day action plan

- Collect passports, recent paystubs, foreign tax returns, and bank statements showing peak balances.

- Run a quick FEIE vs FTC estimate for your most recent tax year (use online calculators or spreadsheets).

- Check aggregate foreign account balances against the $10,000 FBAR trigger and FATCA thresholds for your filing status.

- If self‑employed, estimate Schedule SE liability and check whether a totalization agreement may apply.

- Schedule a consult with our Financial Consultingteam if you have trusts, large accounts, missed filings, or complex income streams.

Useful templates to prepare or download: a FEIE/FTC comparison worksheet, a simple FBAR balance tracker, an example Form 2555 travel and residence log, and a documentation checklist for severing state ties. Expats World’s The Ultimate Pre-Move Checklist for Expats and country and city guides point out local filing quirks and typical documentation asked for by local authorities, and our Wealth Building Essentials resource pages highlight the everyday evidence auditors find persuasive.

When to hire a pro: seek Personal Financial Planning if you have multi‑country income, foreign trusts or companies, substantial account balances, a history of missed filings, or the potential for willful noncompliance. In your first meeting bring the documents listed above, a one‑paragraph summary of your residency history and work patterns, and a clear list of the outcomes you want (compliance, penalty mitigation, tax planning, or a Financial Freedom Blueprint). Expect an initial scoping conversation, an engagement letter outlining fees, and a checklist of records to produce. Professionals can run the exact FEIE vs FTC math, evaluate totalization agreement options, and advise on state domicile strategies.

Wrap — two things to hold on to

First: don’t assume living abroad frees you from U.S. tax obligations. If your worldwide income or account balances cross the thresholds, you must file and report. Second: the right combination of FEIE, FTC, and proper account reporting can often reduce your U.S. tax to zero—but only if you file correctly and keep good records.

Use the The Ultimate Pre-Move Checklist for Expats, keep a single organized digital folder for tax documents, and check Expats World’s country resources for the local filing quirks you’re likely to encounter. When in doubt—especially with large accounts, missed years, or complex cross‑border income—consult a cross‑border tax professional sooner rather than later.